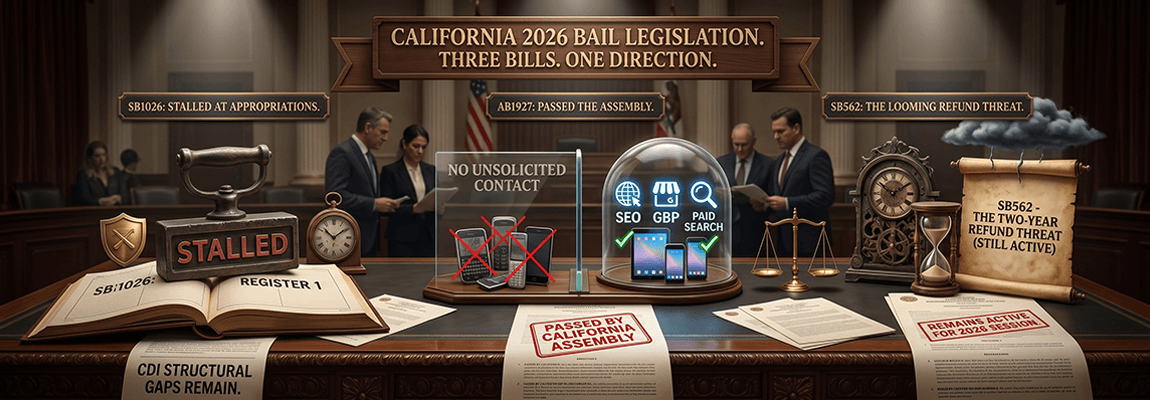

California's 2025-2026 legislative session produced three bills that are directly aimed at bail industry operations. The outcomes are not all the same, but the direction is. Understanding what each bill does, what it does not do, and what the aggregate pattern represents is more operationally relevant right now than tracking any single bill's status.

SB1026 stalled at the Appropriations Committee in May 2026. AB1927 passed the California Assembly and is heading to the Senate. SB562 is a two-year bill, still active and advancing, that targets the economic model underlying every bail premium transaction. One defensive win, one active restriction already clearing the legislature, one financial threat moving through the pipeline. The agencies reading this as a mixed bag are reading it wrong.

Key Takeaways

- SB1026 stalled at Appropriations. The California commercial bail industry has a temporary reprieve this session, but the CDI-identified structural gaps in the BFRA framework remain; a stalled bill is not a closed question.

- AB1927 passed the California Assembly. It prohibits unsolicited outbound contact with arrestee families. SEO, GBP, paid search, and inbound advertising are explicitly protected. The bill eliminates the outbound tactics that many agencies still depend on.

- SB562 would require premium refunds, minus a 2% administrative fee and the premium tax, if charges are never filed or are dismissed within 21 days of arraignment. It is a two-year bill and remains an active threat in 2026.

- AB1927 is a structural tailwind for agencies with dominant inbound infrastructure. When outbound solicitation is restricted, the first agency a family finds organically wins disproportionately. That is an SEO and digital presence problem, not a relationship problem.

- All three bills point at the same structural shift: California is systematically replacing informal bail operations with documented, auditable, compliance-compatible workflows. The agencies building for that environment now are not just staying ahead of legislation; they are building a more durable business.

SB1026 Stalls at Appropriations: What the Outcome Actually Means

SB1026, the Bail Fugitive Recovery Agent Reform Act, passed the Senate Insurance Committee 5-2 on March 25, 2026. It then stalled at the Appropriations Committee in May. For California's commercial bail industry, the stall is a temporary reprieve: the specific requirements in this version of the bill will not take effect this session. That is accurate as far as it goes.

But the context around that outcome matters. CDI is sponsoring SB1026. The California Department of Insurance does not sponsor legislation it intends to abandon. The structural issues the bill targets, the appointment backdating window created by the passive filing model under AB 2043, the absence of direct CDI disciplinary authority over BFRA conduct without a criminal conviction first, the inadequate insurance structure in the existing market, remain exactly where they were before the Appropriations hearing. A stalled bill delays the statutory response. It does not resolve the underlying structural problems CDI was trying to fix.

For agencies in California that rely on independent recovery agents, the practical takeaway is this: the insurance market pressure SB1026 would have created is temporarily off the table. The longer-term direction, toward documented appointment chains, verifiable insurance compliance, and CDI-accessible disciplinary mechanisms, is not. The full breakdown of what SB1026 would have required, and what the regulatory architecture it represents means for agencies building in-house recovery capacity, is covered in our existing deep-dive on the bill.

AB1927: The Solicitation Restriction That Changes How Bail Is Acquired

AB1927, the Bail Consumer Protection Act, passed the California Assembly and is advancing to the Senate. Its core prohibition is direct: bail agents and their representatives cannot make unsolicited calls, send unsolicited texts, or send unsolicited emails to the family members, emergency contacts, or known associates of people who have been arrested.

The bill creates civil penalties for violations. It authorizes license suspension or revocation. It enables enforcement by the Attorney General. And critically, it opens the door for private lawsuits with attorney fee shifting, which means violations become plaintiff-attorney magnets, not just administrative compliance issues.

The text of the bill is explicit about what it does not restrict. Public websites are permitted. General advertising is permitted. Search engine visibility is permitted. Google Business Profiles are permitted. Paid search, programmatic display, organic content, inbound call capture, and any channel where the consumer initiates the contact first, all remain fully available. The target is a specific behavior: using arrest or booking data to directly contact the family of someone who just got arrested before they reach out to you.

That behavior is worth naming plainly, because it describes a tactic the industry has used for decades. Lists of recent arrests, runner-style outreach at jails and courthouses, direct contact with family members identified through booking records, these are the specific practices AB1927 is designed to eliminate. The bill is not a fringe effort. It has the momentum of a legislature that has already watched Google and Meta restrict bail advertising based on exactly this concern.

What AB1927 Means for How Agencies Compete

This is where the operational implications get sharp. When outbound solicitation is restricted, the competitive advantage shifts entirely to inbound visibility. The family member who needs to get someone out of jail at 2 AM is not waiting for an agency to contact them. They are searching. They are on their phone. They are evaluating the first few results they find, making a trust judgment in under two minutes, and calling whoever looks most credible and most available.

The agencies that win in an AB1927 environment are the agencies whose inbound acquisition infrastructure is already dominant: high Google Maps rankings, strong review volume and recency, fast website load times, clear financing visibility, and a phone system that actually answers. Not because those things are new strategic priorities, but because AB1927 eliminates the alternative. You can no longer compensate for weak inbound performance with aggressive outbound outreach. The agencies that have been building inbound infrastructure already have a widening structural advantage; the agencies that have been relying on outbound tactics have a compliance reckoning approaching.

It is also worth noting what AB1927 does not do to programmatic advertising. Behavioral intent targeting, contextual advertising served to anonymous audiences exhibiting active bail-related search behavior, and inbound retargeting campaigns remain lawful. The legal distinction is between targeting identified individuals because of a specific arrest event versus serving advertising to anonymous cohorts based on voluntary commercial intent signals. The former is what AB1927 restricts. The latter is standard digital advertising, and it remains the most effective way to capture bail-market demand at scale.

SB562: The Bill That Attacks Bail Economics Directly

SB562 is the most financially consequential of the three bills, and it is the one that has received the least discussion proportional to its potential impact. The bill is currently a two-year bill: a July 2025 hearing was canceled at the author's request, the bill was held over to the 2026 session, and it remains active. The industry's focus on SB1026 and AB1927 should not obscure the fact that SB562 is still moving.

Here is the core mechanism. Under SB562, if a bail agency writes a bond and one of the following occurs, the court can order the bail agency to refund the premium: the prosecuting agency fails to file charges within 21 days of the bond being posted, or the charges are dismissed within 21 days of the defendant's original arraignment. The refund amount is the full bail premium, minus a 2% administrative reimbursement and the premium tax paid to the state. The remaining approximately 8% to 9% of a standard 10% premium is returned to whoever paid it.

The bail industry's foundational economic argument against SB562 is straightforward: the premium is earned when the bond is posted, because that is when the risk is assumed. The agency accepted liability for the defendant's appearance, posted the bond, completed the underwriting, and arranged financing. The fact that the prosecutor later declines to file charges, or files and immediately dismisses, does not retroactively undo the risk that was assumed or the operational work that was performed. SB562 says that logic does not matter when the outcome meets the triggering conditions.

Why the Second-Order Effects Are the Real Threat

The direct financial exposure from refunds is significant. But the second-order effects on agency operations are where SB562 creates more lasting damage, because they change incentive structures in ways that reverberate through every underwriting decision.

If agencies face refund exposure on bonds where charges are not filed within 21 days, the rational response is to tighten underwriting on cases that pattern-match to those scenarios: first-time charges in categories that prosecutors frequently decline, cases with weak charging documents, defendants whose cases are likely to resolve before arraignment. The agencies that can identify those patterns quickly and accurately will make better decisions. The agencies that cannot will either accept refund exposure they cannot predict or become more conservative across the board, declining bonds they could have written profitably.

The pressure this creates on operational efficiency, underwriting precision, and collections infrastructure is the same pressure that SB562's proponents are probably counting on: if the economics of marginal bonds become less reliable, the agencies with the most sophisticated operational infrastructure will survive and the agencies managing by feel will contract. That is not necessarily the outcome industry advocates would endorse, but it is the likely market structure response if SB562 passes in its current form.

For now, SB562 is a threat to monitor, not a law to comply with. The fact that it is a two-year bill means the author believes the fiscal and policy case can be made with more time. The industry is actively fighting it, which reflects what is at stake. The agencies building operational infrastructure that would make them resilient under SB562 are simultaneously building an operation that survives regardless of legislative outcome.

The Pattern Behind All Three Bills

Taken individually, each of these bills addresses a specific concern: BFRA accountability, consumer protection from solicitation harassment, and premium refund equity. Taken together, they represent a consistent legislative posture that has been building in California for over a decade.

AB 379 in 2012 established the foundational BFRA regulatory framework. AB 2029 in 2012 tightened it. SB 805 in 2025 added conduct requirements. AB 2043 in 2022 created the 437B Notice of Bail Action requirement. SB1026 in 2025-2026 attempted to add CDI formal acknowledgment as a prerequisite for BFRA appointment validity. The pattern is not episodic regulatory activity. It is a sustained, incremental project to bring bail operations into a documentation and accountability framework that California's regulatory agencies can actually oversee.

AB1927 is part of the same project on the acquisition side: eliminating the informal, relationship-driven, contact-list-dependent tactics that have historically characterized bail marketing and replacing them with the kind of inbound, consent-based, consumer-initiated contact that is consistent with every other regulated industry's advertising rules. SB562 extends the same logic to bail economics: if the consumer outcome is poor enough, early enough, the premium should not be fully retained.

The agencies that read these bills as separate policy debates are missing the forest for the trees. California is systematically restructuring bail operations around the assumption that agencies will be using software that creates auditable records, not spreadsheets or informal workflows that cannot be verified. The compliance infrastructure that sureties and regulators are increasingly expecting is not optional for agencies that want to operate at scale in this environment.

What to Do Now

For SB1026: the stall buys time. Use it to build the documentation infrastructure, the verifiable BFRA appointment chains, the insurance verification workflows, the CDI-accessible records, that the bill was requiring. Not because the bill is coming back next session specifically, but because the agencies that build this infrastructure are building a more defensible operation regardless of what CDI does next.

For AB1927: the bill is advancing. Treat the outbound solicitation tactics it prohibits as already unavailable for planning purposes. The correct response is not to wait for the Governor's signature to start investing in inbound infrastructure. It is to build the local search dominance, the review velocity, the response speed, and the conversion infrastructure that makes your agency the one a family finds and trusts first, before the restriction is legally in force and your competitors are scrambling.

For SB562: monitor it, model the exposure if it passed in current form, and build the underwriting precision that reduces your refund risk regardless. An agency that can identify within 48 hours whether a new bond is likely to hit the 21-day no-charges scenario is an agency that has better underwriting intelligence across the board. The operational technology stack that produces that kind of intelligence is the same stack that makes every other part of your operation more defensible under regulatory scrutiny.

Three bills. One direction. The agencies building for that direction now are not waiting for legislation to force the issue. They are building the most durable version of their business, and that happens to also be the version that is most compliant, most auditable, and most defensible when the next bill arrives.

California's regulatory environment is being built on the assumption that bail agencies run documented, auditable, compliance-ready workflows. IntelliBail is the operational platform built for exactly that environment: underwriting intelligence, active bond management, collections automation, inbound acquisition infrastructure, and the kind of systematic record-keeping that holds up under surety scrutiny and regulatory review.

See the platform →