Your surety is not just tracking your loss ratio anymore. Tightening regulation has added new items to the evaluation checklist, and the agencies that know what those items are and have documentation ready are positioned differently at every portfolio review than the ones scrambling to reconstruct records on request.

The regulatory environment for bail recovery operations is changing in ways that directly affect surety evaluation criteria. Understanding the new scrutiny patterns is not optional for agencies that want to maintain and improve their surety relationships.

Key Takeaways

- Sureties are not passive counterparties. They track agency performance continuously and adjust power books, collateral requirements, and premium structures based on observable metrics. Tightening regulation creates new metrics they are now actively evaluating.

- As state-level regulation of bail fugitive recovery operations tightens, sureties are adding BFRA vetting documentation to their standard audit checklist. Agencies that have already built systematic vetting processes answer those questions with evidence; agencies that have not scramble to reconstruct compliance records under audit pressure.

- Compliance posture is a surety relationship variable, not just a regulatory obligation. Agencies that demonstrate proactive compliance management before being asked negotiate from a stronger position than agencies that respond reactively to audit inquiries.

- The documentation audit is a specific, enumerable list. Agencies that build an audit-ready compliance file now will answer surety questions in minutes rather than days, and that speed difference registers in how sureties categorize agency risk.

- The regulatory tightening in California follows a pattern that has repeated across multiple jurisdictions. Agencies in other states should be building compliance infrastructure that reflects the likely regulatory trajectory, not just current requirements.

What Sureties Actually Track

The established metrics have not changed. Loss ratio remains the primary performance indicator, measured as forfeiture losses divided by written premium. Power book utilization, payment history, and collateral coverage are still tracked. These are the foundational variables that determine power book size, collateral requirements, and premium rates.

But these metrics alone are no longer sufficient. Sureties operate risk-adjusted portfolios across dozens or hundreds of agencies. A single agency with deteriorating compliance signals affects the surety's own regulatory exposure, not just that agency's performance. When state regulation tightens, sureties respond by tightening evaluation criteria.

The surety is not just evaluating past performance. They are evaluating operational maturity and the likelihood that the agency will create future compliance problems. One of the most significant differentiators in a surety evaluation is the presence of documented processes versus informal management. Agencies that document recovery timelines, BFRA vetting steps, forfeiture deadlines, and indemnitor engagement show institutional readiness. Agencies that manage by feel show operational risk.

This distinction affects everything. An agency with documented compliance processes can answer surety questions with evidence. An agency without documentation can only offer explanations. One takes minutes; the other takes weeks and still leaves doubt.

The New Scrutiny Patterns

Before tightening regulation, sureties primarily asked about financial performance metrics. Loss ratio, payment history, collateral coverage. These remain important. But the questions in surety audit cycles have shifted.

The operational compliance questions that are now standard include: How do you vet the recovery agents you contract with? Can you confirm their current insurance status? What is your pre-apprehension notification documentation process? How do you track open forfeitures against their summary judgment deadlines? What does your indemnitor engagement record look like per bond?

These questions have become more specific and more routine as state-level regulation of bail fugitive recovery operations has tightened. Sureties are tracking whether agencies understand the regulatory environment in their operating jurisdictions and whether their operational processes reflect it. Agencies with elevated summary judgment exposure see the most pressure in these audit cycles.

Agencies that can answer these questions with documented evidence rather than verbal assurances register differently in risk evaluations. Evidence creates certainty. Verbal assurance creates questions, and follow-up questions, and delays.

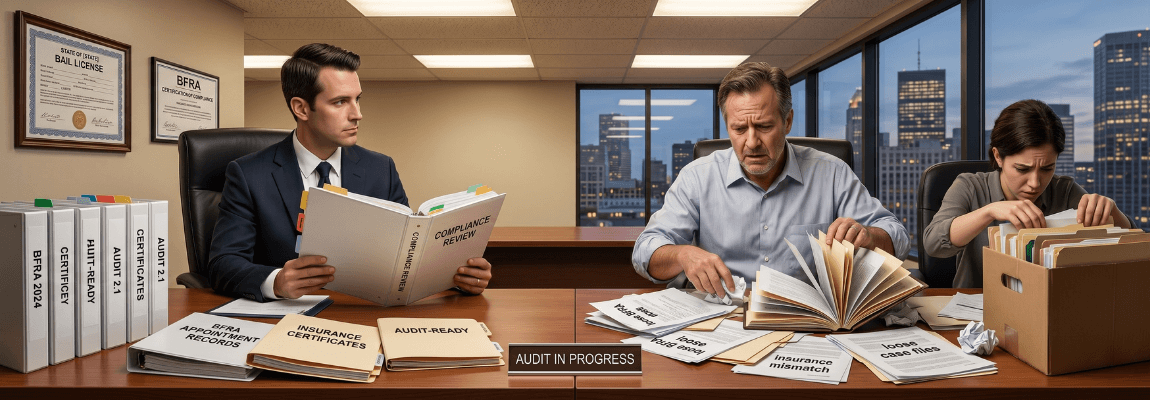

BFRA Vetting in the Compliance Checklist

The BFRA vetting process that sureties are increasingly requiring is specific and enumerable, and it applies regardless of jurisdiction:

Verify the BFRA holds a current bail fugitive recovery license in every state where they will be operating on your bonds. Check the license number against the state regulatory database directly, not just the agent's word. Confirm that any required Notice of Appointment has been filed with the appropriate regulator and, where required, acknowledged before the appointment is treated as effective. Verify the BFRA maintains standalone liability insurance rather than relying on the agency's general policy, and that the policy covers the full term of the appointment. Confirm the policy is written by a carrier admitted in the operating state. Request copies of pre-apprehension notification documentation as cases are worked, and retain those records at the bond level.

Agencies that are running this checklist now will have the documentation habit established before it becomes a surety requirement. Agencies that are not will be building documentation processes under pressure, answering audit questions reactively instead of proactively.

The distinction matters for surety relationships. An agency that can produce a comprehensive BFRA vetting file demonstrates operational maturity and anticipatory compliance thinking. An agency that scrambles to assemble documentation after being asked demonstrates reactive management. Sureties weight that difference in their risk models.

What Your Documentation Should Look Like

The ideal compliance file is organized at the bond level, not the agency level. When a surety auditor asks a question about a specific bond, you should be able to pull one file and find the answer immediately. Purpose-built bail management platforms structure documentation this way by design; most agencies building this manually in spreadsheets discover the gaps only under audit pressure.

Bond-level documentation that should exist for every active bond includes: application and indemnitor documentation; any collateral receipts and valuation; post-release check-in records if applicable; FTA occurrence documentation with date and initial response steps; BFRA appointment records with regulator acknowledgment timestamp where required; recovery case notes and status updates; pre-apprehension notification records with written content; forfeiture notice from court with date received; deadline tracking showing the jurisdiction-appropriate appearance period timeline; legal action records if motion practice was pursued; exoneration or summary judgment outcome documentation.

This is not bureaucracy for its own sake. This is the record that answers every surety question in a future audit. Agencies lacking bond-level organization often discover their compliance blind spots only when a surety audit forces them to assemble the file under pressure.

Turning Compliance Into Leverage

The agencies with the strongest surety relationships are not just compliant. They demonstrate compliance proactively, and that demonstration changes how sureties evaluate them.

What that looks like practically: quarterly performance summaries shared with surety contacts before they ask; forfeiture rate trend data with context on how it compares to prior periods; documentation of any forfeiture that occurred and what recovery steps were taken; proactive notification of any compliance changes or new operational processes.

This approach changes the tone of surety interactions. Instead of a reactive audit where the agency is answering questions after the fact, it becomes a collaborative performance review where the surety sees the agency's operational maturity firsthand. Agencies with the strongest surety relationships treat compliance documentation as relationship currency, not regulatory overhead. That posture shapes every surety interaction.

Consider the role of forfeiture documentation. Agencies with low summary judgment rates have documentation that explains why. Recovery processes that are systematic and tracked. Legal evaluations completed before the deadline window closes. When that data is shared with the surety, it registers as risk mitigation. The agency is not hiding from forfeitures; it is managing them. That distinction affects power book increases, collateral flexibility, and long-term relationship sustainability.

Build the Infrastructure Before You Need It

The argument for building compliance infrastructure before it becomes required is historical. Every significant regulatory update to bail industry operations has expanded documentation requirements rather than reduced them. The agencies that meet current requirements reactively are perpetually behind; the agencies that build operational documentation habits ahead of requirements find that compliance arrives as a byproduct of how they already operate.

That pattern holds across jurisdictions. The states that have tightened BFRA oversight have done so in escalating steps, each making the prior requirements a floor rather than a ceiling. Building the documentation infrastructure now means the next regulatory update, wherever it comes from, requires adaptation rather than reconstruction.

The documentation process that tracks BFRA vetting, recovery timelines, forfeiture deadlines, and indemnitor engagement works in every jurisdiction. The questions a state regulator asks during an audit are the same questions a surety asks during a portfolio review. Building the process once satisfies both.

The goal is not to pass an audit. The goal is to operate in a way where an audit is not a threat. Agencies that document their operations as a matter of course build the compliance record as a byproduct of running the agency well, not as a separate compliance exercise. That operational maturity is visible in every surety interaction and affects every relationship outcome.

Surety audit questions about recovery operations and compliance documentation are now routine. IntelliBail maintains the compliance record across every bond, BFRA appointment, and regulatory checkpoint, so the documentation your surety needs is already organized when they ask for it.

See the full platform →