Most people think a bail bond is a transaction. A defendant is arrested, bail is set, a bondsman writes the bond and collects a premium. Simple. Clean. Done. Experienced bail agents know the real story begins after the bond is written, and that what happens next determines whether the agency made money or lost it.

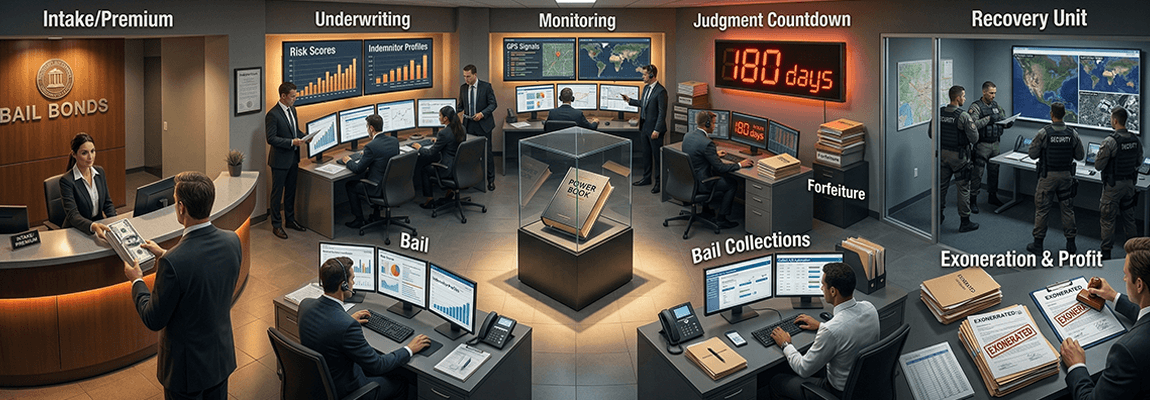

Every bond that leaves the office enters a financial lifecycle. That lifecycle has seven distinct phases, and at each one, money either flows toward the agency or away from it. The agencies that consistently operate at sub-5% forfeiture rates and healthy loss ratios are not just writing better bonds. They are managing this lifecycle deliberately, at every phase, from the first underwriting call through exoneration. Understanding each phase is the difference between managing a bail agency and just running one.

Key Takeaways

- A bail bond is not a transaction. It is a financial lifecycle with seven distinct phases, each carrying distinct risk and profit implications for the writing agency.

- Most bond losses are determined before the bond is ever written. The underwriting decision sets the risk trajectory for every phase that follows.

- A failure to appear does not immediately cost the agency money. It starts a countdown. How the agency manages the appearance period determines whether that countdown ends in recovery or in a court judgment against the surety.

- Summary judgment converts a recoverable forfeiture into a fixed liability. The agencies with the lowest SJ rates operate deadline-management systems, not reactive recovery operations.

- The agencies that consistently outperform are not better at reacting to bad outcomes. They are better at seeing risk early enough to shape it, across an entire portfolio of open bonds, not case by case.

The First Decision: Risk Before the Bond

Every dollar the agency loses on a bad bond can be traced back to a decision made before the bond was written. That is not hindsight. It is the mechanism. The underwriting decision sets the risk trajectory for everything that follows: the defendant's likelihood of appearing in court, the indemnitor's capacity to ensure they do, and the collateral position available to absorb a loss if the bond goes sideways.

The variables that separate low-risk bonds from high-risk ones are not mysterious. Indemnitor employment stability, residential continuity, the nature of the relationship between indemnitor and defendant, prior failure-to-appear history on the defendant's record, charge severity, collateral position relative to face value, and whether the premium structure creates a financial stake the indemnitor is motivated to protect throughout the bond term. Agencies that evaluate these variables systematically, through a structured intake protocol applied consistently to every bond, outperform those that rely on agent intuition alone. Not because intuition is worthless, but because intuition is inconsistent at scale and cannot be audited when a bond goes wrong.

The structural challenge is economic: writing the bond earns the premium. Declining earns nothing visible that day. That asymmetry creates pressure toward yes, and it accumulates faster than the visible forfeiture rate suggests. The costs of an over-written book show up later, in forfeiture reserve draws, power book reductions, and surety relationship friction that is far more expensive than the premium that was collected. Agencies that build the discipline to decline marginal bonds consistently find that the lost premium revenue is a fraction of what those bonds would have cost downstream.

The intake decision is also the only phase in the lifecycle where the agency has full control. Every subsequent phase involves variables the agency can influence but not determine: defendant behavior, indemnitor responsiveness, court scheduling, recovery logistics. The underwriting decision is entirely within the agency's authority. Treating it with commensurate rigor is the foundation of every phase that follows.

The Hidden Phase: Defendant Behavior After Release

Between signing and the first court date, most agencies lose operational visibility entirely. The premium is collected. The bond is executed. The file is moved to a passive status or closed outright. And then nothing happens operationally until the court date arrives, or does not.

This gap is where the financial trajectory of most bonds is actually decided.

Most defendants who ultimately fail to appear show observable signals well before the court date: payment plans that begin slipping, phone numbers that change without notification, indemnitors who become progressively harder to reach, address histories that shift without corresponding updates to the bond file, communication patterns that move from cooperative to evasive. These signals are visible if someone is systematically looking for them. Most agencies are not looking systematically, because the operational infrastructure to do so requires deliberate design, and most agencies have never built it. The framework that prevents failures to appear is almost always an active one, not a passive waiting game.

The agencies with the lowest failure-to-appear rates are not just better at selecting defendants. They are operationally present during the bond term in ways that keep defendants accountable and give the agency early warning when something shifts. Court date reminders coordinated through the indemnitor. Payment plan touchpoints that double as relationship maintenance. Systematic outreach protocols that create a consistent presence across the entire bond term rather than a blank period between signing and court. Indemnitor engagement throughout the bond term is the most underused prevention lever in bail, and the agencies that use it deliberately operate in a fundamentally different risk environment than those that do not.

None of this is surveillance. It is relationship management applied at a consistent cadence, and it accomplishes something underwriting alone cannot: it keeps the indemnitor financially and emotionally engaged throughout the bond term, which is the single most valuable asset the agency has when a defendant begins showing signs of flight risk. An engaged indemnitor is a recovery asset. A disengaged indemnitor is an obstacle.

The First Breaking Point: Failure to Appear

A failure to appear does not immediately cost the agency money. It starts a clock.

When a defendant misses a scheduled court date, the court issues a forfeiture: a formal declaration that the surety is financially liable for the full bond amount. With that, an appearance period opens. This is the window during which the agency and surety have the opportunity to resolve the situation before that liability becomes an enforceable court judgment. The window is typically 180 days from the date of forfeiture, though the exact timeline is jurisdiction-specific. How that window is used, or wasted, determines the financial outcome of the bond. The mechanics of how and why forfeitures unfold follow patterns that experienced agencies recognize and act on systematically.

The agencies that recover defendants within the appearance period are not necessarily better at fugitive tracking. They are better at starting immediately. The first two to three weeks after a missed appearance are the highest-value recovery window in the lifecycle. Co-signers are still reachable and responsive. The defendant's network has not yet adjusted to the fact that they are being sought. Location signals are fresh. The indemnitor's financial exposure is still vivid enough to motivate cooperation, and the social pressure that makes voluntary resolution possible has not yet dissipated.

Agencies that delay serious recovery work until week 10 or later are not just losing time. They are losing the period in which recovery is most achievable at lowest cost. By the time a case reaches the four- or five-month mark without resolution, the operational reality has changed: indemnitors have often moved on emotionally and financially, networks have tightened, and the leverage available is legal rather than relational. That shift is expensive in both time and recovery cost, and it is largely preventable through early, systematic activation.

The Financial Cliff: Forfeiture and Summary Judgment

If the appearance period closes without resolution, the court enters summary judgment: a formal ruling that converts the forfeiture into an enforceable judgment against the surety. At that point, the problem changes in kind, not just degree. A recoverable situation becomes a fixed liability, and the options that were available for the previous 180 days are gone.

The immediate financial consequence is the full bond amount becoming a draw against the agency's forfeiture reserve with the surety. For a $50,000 bond, that is a $50,000 line item. For agencies carrying multiple open FTAs without systematic deadline tracking, those draws do not arrive one at a time. Understanding what summary judgment actually does to an agency's reserves and surety relationship is one of the most operationally important things a bail agent can know, and one of the least discussed until it is too late.

The cascade that follows a summary judgment extends beyond the immediate financial hit. Recovery expenses incurred after the judgment date are no longer collectible from the indemnitor; those costs come out of the agency's pocket. The agency's loss ratio, the metric sureties use to evaluate the writing relationship, deteriorates. And in many jurisdictions, a surety corporation that carries five or more unresolved defaults in a county cannot place new bonds in that county, which directly restricts the agency's ability to write in that market. That threshold is not theoretical. For agencies with no deadline tracking and an active book, it is closer than it appears.

Sureties respond to elevated loss ratios in graduated ways: power book limits are reduced, collateral requirements increase, and preferred-agency status is withdrawn. The surety relationship is the agency's most critical business asset, and it is also the asset most directly damaged by summary judgment accumulation. The adjustments compound: lower power books mean less premium written, which means less revenue to absorb the next forfeiture. The cycle accelerates once it starts, and reversing it is far harder than preventing it.

The agencies with consistently low SJ rates do not manage forfeitures by feel. They maintain a visible deadline for every open FTA, run tiered escalation protocols based on time elapsed rather than case progress, and evaluate legal intervention options before the appearance period closes, not after the judgment enters.

The Race Against Time: Fugitive Recovery

Recovery is intelligence work, not pursuit.

The popular image of bail recovery as a physical operation, tracking and apprehending defendants across state lines, is real but secondary to what actually determines outcomes. Successful recovery is almost always a product of relationship leverage activated early and applied systematically: an indemnitor who has more to lose from the agency pursuing collections than from producing the defendant, a family network that responds to structured outreach, a community footprint that makes location less difficult than the elapsed time suggests. Physical recovery is the final step in a process that begins with information gathering and ends when relational leverage has been exhausted. The operational infrastructure behind effective FTA management is built around this intelligence-first model, not the other way around.

Time is the compressing variable throughout this phase. Every week that passes narrows the relationship window: phone numbers change, indemnitors disengage emotionally, financial pressure fades as they distance themselves from the obligation, and social networks close around a defendant who has been missing long enough for people to stop being surprised. The trajectory of most FTA cases is not determined by the quality of the recovery effort in week 14. It is determined by the quality of the indemnitor relationship at week 1 and the speed with which the agency activated it.

Agencies that manage this phase systematically treat recovery as an extension of the indemnitor relationship that was built during the bond term. The indemnitor who received consistent check-in contact throughout the bond is a fundamentally different starting point than the indemnitor who has had no contact since signing and now faces an aggressive collection posture from an agency they barely remember. The former has context, trust, and a shared sense of investment in the outcome. The latter has an adversarial relationship with a creditor. The outcome gap between those two starting points is large, and it is set long before the FTA occurs.

The Long Tail: Bail Collections

Even when the defendant appears in court and the bond exonerates on schedule, the financial lifecycle of that bond may not be over.

The second revenue battle in bail is collections: premium due on installment plans, unpaid balances from co-signers, and the broader pattern of delinquent accounts that quietly erodes revenue without triggering any of the alarm signals that a forfeiture would. A defendant who appears in court on time is a resolution from an operational standpoint. A defendant who appears on time while their indemnitor is 90 days delinquent on a split-pay plan is a different financial reality entirely: one that generates no visible urgency, costs ongoing staff time to manage, and quietly erodes premium revenue in ways that only become clear in aggregate. The hidden revenue drain that occurs after the bond is written is one of the most underdiscussed financial risks in bail agency operations.

The scale of this problem is larger than most agencies measure. Installment plans that slip into delinquency carry a compounding cost: the uncollected balance, the staff hours required to pursue it, the legal costs if it escalates, and the opportunity cost of capital tied up in receivables that should have been closed months earlier. Agencies that have not built a structured collections process absorb these costs as general overhead, which makes them nearly invisible in any particular accounting period and fully visible only when loss ratios are calculated at the surety level. By then, the damage is done.

The agencies that control their collections outcomes are not necessarily more aggressive; they are more structured: tiered escalation based on days delinquent, defined milestones where formal notice triggers automatically, and a clear decision framework for when a delinquent account becomes a referral. A structured collections tier strategy turns the outcome of a delinquent account from open-ended to predictable, which is the difference between managing receivables and hoping they resolve. Systematic indemnitor collections management is the operational layer that makes that structure operational rather than theoretical.

The Reality Most Agencies Never Measure

Ask most bail agency operators how many open FTAs they are currently carrying within 60 days of their summary judgment deadline, and they cannot answer the question quickly. Ask how many delinquent payment plans are past 90 days, and the same uncertainty returns. Ask what their current loss ratio is relative to their surety's preferred threshold, and few know the number without pulling a report they do not check on a regular cadence.

This is not a failure of attention or effort. It is the predictable output of managing a complex portfolio of risk exposures case by case, without the aggregate visibility that would make systemic patterns obvious before they become expensive.

Elite agencies operate with a fundamentally different frame: portfolio risk, not case management. Every active bond is a position with a defined risk profile. Every open FTA is a countdown with a known deadline. Every delinquent account is a probability curve rather than an isolated file. This framing changes what gets measured, what gets escalated, and what gets reviewed at the agency level on a regular basis, rather than surfacing only when a threshold is already breached and the remediation options are narrowed.

The difference is not just operational efficiency. It is the difference between reacting to problems after they become expensive and identifying them when they are still cheap to resolve. An FTA at day 14 of a 180-day appearance period is a recoverable situation with every tool still available. The same FTA at day 160 is a crisis. An indemnitor 15 days delinquent is a brief follow-up call. The same indemnitor at day 120 is a legal matter with compounding cost. In both cases, the problem began at a moment when it was manageable, and it reached crisis through a combination of elapsed time and insufficient visibility. The agencies that catch it early are not working harder. They are working with better information, applied earlier.

The full operational infrastructure that makes portfolio-level visibility systematic is the same infrastructure that drives lower forfeiture rates, lower SJ rates, and stronger surety relationships across the book: active tracking from the moment a bond is written through exoneration, with deadline fields and risk signals that create urgency before an open file becomes an uncontested liability.

IntelliBail maps the full financial lifecycle of every bond in a single operational view: structured intake, court date tracking, FTA deadline visibility, recovery escalation, and collections management. Portfolio risk across the full book, in real time, not in the rearview mirror.

See the full platform →The bail industry has always run on relationships, judgment, and experience. That does not change. But the financial lifecycle of a bail bond is longer and more operationally complex than the single-transaction frame suggests, and managing it well at scale requires more than good instincts applied to individual cases.

The agencies that thrive over the long term combine instinct with system: operational infrastructure that keeps every bond visible from intake through exoneration, surfaces risk signals before they compound, and manages every phase of the lifecycle with the same deliberateness applied to the first underwriting call. The financial lifecycle is not a mystery. It follows observable patterns at every phase. The agencies that understand those patterns, and build their operations around them, rarely encounter losses they could have seen coming.